The Strait of Hormuz disruption has tested the region’s supply chains, but the UAE’s stockpiles, infrastructure, and trade strategy continue to support resilience and long-term growth.

Published in Abu Dhabi, 21 APR 2026 01:45 am (GST)

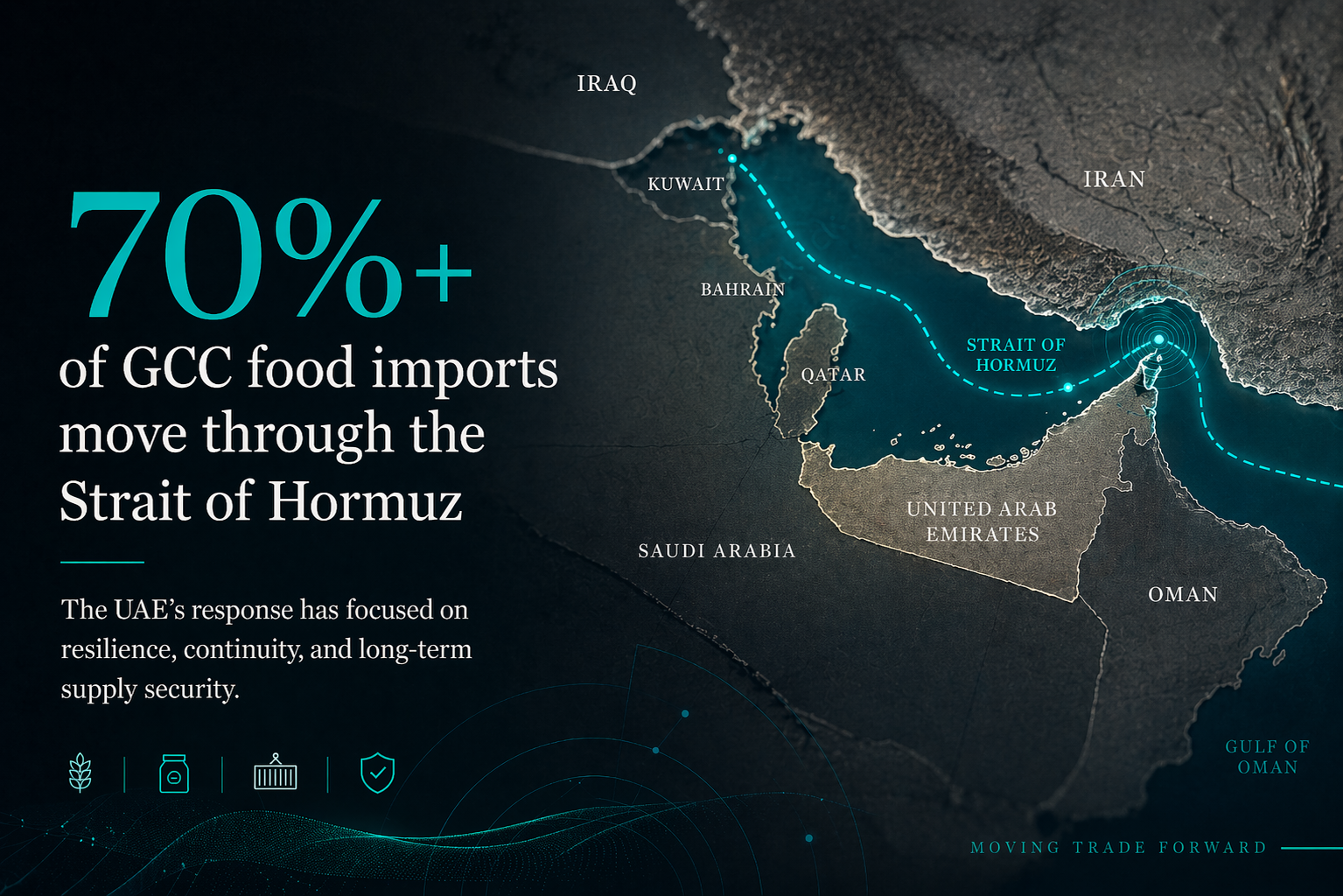

The closure and stop-start reopening of the Strait of Hormuz has rightly dominated headlines, but the deeper commercial story for the GCC is not only about crude. It is about the commodities that sit behind daily stability, food security, industrial continuity, and trade confidence: wheat, sugar, and fertiliser. In my view, these are some of the most important commodities to watch if you want to understand how the Gulf, and especially the UAE, is navigating the current environment.

The facts are clear. The GCC is heavily import-dependent for food, with Reuters reporting the Gulf states are around 90% reliant on food imports and that more than 70% of GCC foodstuffs are imported through the Strait of Hormuz. That means any disruption at Hormuz is not simply a shipping problem. It is a direct pressure point on wheat flows, sugar supply chains, edible staples, and the timing and cost of getting goods onto shelves and into industrial networks.

Fertliser is the other major pressure point, and this is where the current situation becomes even more strategic. Reuters reported in March that one-third of global fertiliser trade passes through the Strait of Hormuz, while energy can account for as much as 70% of fertiliser production costs. That matters because fertiliser is not a side issue. It is central to agricultural output, and Reuters also noted that about half of the world’s food is grown using fertiliser. When fertiliser moves are disrupted, the impact travels far beyond one port or one shipment. It affects planting decisions, crop economics, food prices, and procurement strategies across multiple regions.

The market has already shown how quickly this pressure can build. Reuters reported that urea prices were already nearing $700 per tonne in late March, almost 50% above pre-bombing levels, and by mid-April Indian import offers had climbed to around $1,000 per tonne, roughly double the levels seen two months earlier. That is not noise. That is a major cost shock moving through the agricultural chain.

Sugar is another commodity that deserves much more attention in this environment. Reuters reported that the Gulf imports roughly 10% of the world’s raw sugar through the Strait of Hormuz each year, while exporting about 5% of global refined sugar through the same chokepoint. Dubai’s Al Khaleej Sugar refinery alone accounts for nearly 4% of the world’s annual imports of raw sugar and more than 4% of global refined sugar exports, underlining how strategically relevant the UAE remains within this market.

So yes, the risks are real. The ongoing situation remains unstable. Reuters reported today, 20 April 2026, that even where temporary openings have been announced, shipping through the Strait remains highly uncertain, with traffic still slowed to a trickle and recovery to pre-war norms likely to take months, and possibly years, even if the fighting eases. Reuters also reported that around 13 million barrels per day of oil and roughly 300 million cubic metres per day of LNG have been trapped inside the Gulf, while the willingness of shipowners, insurers, and tanker operators to re-enter normal patterns remains a major constraint. That matters for non-oil commodities too, because insurance, freight pricing, route availability, and vessel confidence do not operate in silos.

But this is where the UAE’s position stands out.

The UAE has not approached this challenge passively. It has spent years building for exactly this kind of volatility. Reuters reported in March that the UAE said its strategic reserves of vital goods covered four to six months of needs, while government agencies urged residents to report unjustified price rises. The Ministry of Economy and Tourism has also confirmed a strategic stockpile of essential goods that can cover market needs for up to six months, and has prohibited price increases on nine key commodity categories, including sugar and wheat, without prior approval.

That is not just optics. It is policy-backed market management. And the logistics side matters just as much. Reuters noted that the UAE’s Fujairah grain silos, opened on the Indian Ocean coast outside the Strait, have capacity of roughly 300,000 metric tonnes and were strategically located specifically to provide routing flexibility when the maritime environment tightens. That does not remove all vulnerability, but it does provide a serious buffer and a clear example of forward planning.

The UAE has also moved operationally, not just structurally. The Ministry of Climate Change and Environment said on 18 March 2026 that it had put in place a comprehensive proactive plan to ensure the uninterrupted flow of food, agricultural, and animal consignments through all UAE entry points, including fast-track clearance channels and reinforced specialist teams. The ministry reported that 441,574 heads of livestock had already been received across 1,454 consignments since the start of the year to meet market demand, while stressing uninterrupted food flows and full logistical integration across major entry points.

That is why I think the correct reading of the current moment is not panic, but differentiation.

There has clearly been a trade slowdown in certain channels. Reuters reported that Fujairah’s marine fuel sales fell to a record low of 158,852 cubic metres in March, down more than 70% from February and from the same month a year earlier. Reuters also reported that the UAE non-oil PMI fell to 52.9 in March from 55.0 in February, its weakest pace in nearly four years. But the same Reuters report made an important point: the PMI remained in growth territory, and for many firms order books remained resilient and output still expanded.

That distinction matters. Slower is not the same as broken.

In fact, the broader evidence still points to a business environment that remains active and investable. Dubai Chambers reported that 2,709 new companies joined the Dubai Chamber of Commerce in March 2026, reflecting continuing investor appeal even amid the current backdrop. Earlier this year, Reuters also reported that new registrations at DIFC rose by nearly 40% in 2025 to 1,525, with the total number of active firms reaching around 8,840. That does not happen in a market the world has written off. It happens in a market that global capital still sees as organised, credible, and capable of recovery.

The policy response has been equally telling. Reuters reported that Dubai approved AED 1 billion in economic facilitation measures beginning on 1 April 2026, designed to support business flexibility, improve preparedness, and help businesses and families navigate the current conditions. This is the sort of intervention that does not solve geopolitics, but does reinforce confidence where it matters most: on the ground, in commercial behaviour, in financing conditions, and in operational continuity.

From a forward-looking commodity perspective, my view is straightforward.

Wheat will remain central because food security is still the most politically and economically sensitive issue in any import-dependent region. Buyers will continue to prioritise reliability, lead times, and reserve-backed supply over chasing the last marginal discount. The UAE is likely to deepen relationships with diversified origin markets and keep investing in strategic storage and routing flexibility.

Sugar will remain important because the UAE already plays a meaningful role in regional and global refining and re-export flows. In an uncertain maritime environment, established operators with infrastructure, stocks, and trade credibility become more valuable, not less. I expect the market to reward players who can offer clean paperwork, real logistics optionality, and serious execution discipline.

Fertiliser may prove the most underestimated of the three. If Hormuz volatility persists, fertiliser prices could remain structurally firmer for longer than many buyers want to believe. That has implications not only for agriculture in importing regions, but also for how GCC-linked traders think about inventory timing, supply commitments, and cross-border agricultural exposure.

And more broadly, I believe the UAE will continue to strengthen its role as a risk-managed commodity platform, not just a transit point. Its CEPA strategy is explicitly designed to build on its position as a global trade and logistics hub, and the country is still projected by the IMF to grow by 3.1% in 2026 despite the shock, with regional growth expected to rebound sharply to 4.8% in 2027 if trade routes and production normalise.

So yes, the region is under pressure. Trade has slowed in places. Costs have risen. Freight, insurance, and timing risk are all very real. But the headline that matters most is this: the UAE is not standing still inside the disruption. It is absorbing pressure, using infrastructure, using policy, using reserves, and using trade relationships to keep business moving.

That is why I remain positive.

Not blindly positive. Not sales-brochure positive. But commercially positive.

Because when volatility hits, the markets that prosper are rarely the ones with no exposure. They are the ones with the best preparation, the best systems, and the most credible route back to scale. On that basis, the UAE still looks one of the strongest stories in the region.

The region is under pressure, but pressure also reveals which markets are prepared. In my view, the UAE remains one of the best-positioned trade and logistics environments in the Gulf, not because it is untouched by disruption, but because it has invested in the infrastructure, reserves, and commercial systems needed to keep moving through it.

Leon Henderson

CEO, Auctora Trade Group