Haberler ve Güncellemeler

An in-depth Auctora Trade Group market insight examining how disruption around the Strait of Hormuz is affecting key GCC commodities including wheat, sugar, and fertiliser, and why the UAE’s infrastructure, reserves, and trade strategy continue to support resilience, continuity, and long-term growth.

Global sugar market update April 2026. Explore sugar prices, Brazil ethanol impact, India supply pressure, export flows, and soft commodities trade insights. UAE Consutlants

Supply Chain Shifts, OPEC+ Moves, and the UAE’s Energy Strategy Published in Abu Dhabi, 02 Feb 2026 11:59 am (GST) At the start of February 2026, the global oil market stands at a crossroads. Crude prices are caught between two opposing forces. On one side, a growing supply surplus is exerting downward pressure. On the other, geopolitical tensions continue to inject volatility into pricing. Brent crude has recently approached the $70 per barrel level amid renewed U.S.–Iran friction, even as consensus forecasts point to average pricing in the low $60s for the year ahead. This complex environment is being shaped by three converging dynamics: structural shifts in global supply chains, recalibrated strategy within OPEC+, and long-term energy transition planning led by major producers such as the UAE. Global Oil Supply Chain Shifts T he global oil supply chain has been materially reshaped by geopolitics, sanctions, and changing demand centres. Following Russia’s invasion of Ukraine, crude trade flows were rapidly reoriented. By 2024, approximately 81 percent of Russian crude exports were flowing into Asia, primarily China and India, compared with around 40 percent in 2021. Europe’s share fell to roughly 12 percent, down from nearly half prior to the conflict. European refiners responded by diversifying supply, increasing imports from the Middle East, Africa, and the Americas. This diversification improved resilience but raised transport costs and extended supply routes. Key global shifts include: China , now the world’s largest crude importer, imported approximately 11.1 million barrels per day in 2024. Russia has become its largest single supplier, supported by discounted pricing and long-term bilateral trade arrangements. India dramatically expanded imports of Russian crude, which now account for roughly one-third of its total oil intake. This shift strengthened India’s refining margins but triggered political pressure from Western governments throughout 2025. Europe , following its embargo on Russian oil, sources roughly one quarter of crude imports from Africa and over one fifth from the United States. Middle Eastern producers, including the UAE, have also increased volumes into European markets. The United States remains a substantial crude importer at approximately 6.6 million barrels per day, despite its position as a top global producer. The U.S. primarily imports heavy crude grades from Canada to meet refinery specifications, while exporting lighter grades and refined products. Beyond trade redirection, the supply landscape itself is expanding. New non-OPEC producers are gaining influence. Brazil, Guyana, and Canada are collectively expected to add around 2.4 million barrels per day of supply by 2026, intensifying competition and reinforcing a well-supplied global market. At the same time, oil demand growth continues to tilt eastward. Consumption in Europe and Japan remains subdued due to efficiency gains and slower growth, while China and India continue to drive incremental demand. This reinforces Asia’s central role in global oil flows and strategic planning.

A shift toward structured supply, disciplined capital allocation, and clearer pricing signals for producers and buyers alike. Published in Abu Dhabi, 07 January 2026 11:49 am (GST) As the global energy sector moves into 2026, one thing is becoming increasingly clear: oil markets are entering a more structured and disciplined phase. After several years marked by sharp volatility, geopolitical shocks, and shifting narratives around energy transition, the current environment is defined less by uncertainty and more by strategic positioning. Demand has proven resilient across key sectors including aviation, petrochemicals, power generation, and emerging markets. At the same time, supply growth has remained controlled, with producers prioritising capital discipline and long-term stability over volume expansion. This balance is setting a constructive foundation for the year ahead. In the Middle East, and particularly the UAE, energy markets are benefiting from clarity of direction. National oil companies continue to invest across upstream, downstream, and infrastructure projects while maintaining a pragmatic approach to energy transition. Rather than moving away from hydrocarbons, the focus is on optimisation, efficiency, and reliability. This approach is increasingly attractive to global buyers seeking secure, long-term supply in a fragmented world. Recent geopolitical events have reinforced the importance of jurisdictional stability rather than disrupting market fundamentals. While headlines can introduce short-term volatility, the oil market has shown an ability to absorb shocks without significant dislocation. This reflects both improved supply management and a deeper understanding among market participants of underlying demand dynamics.

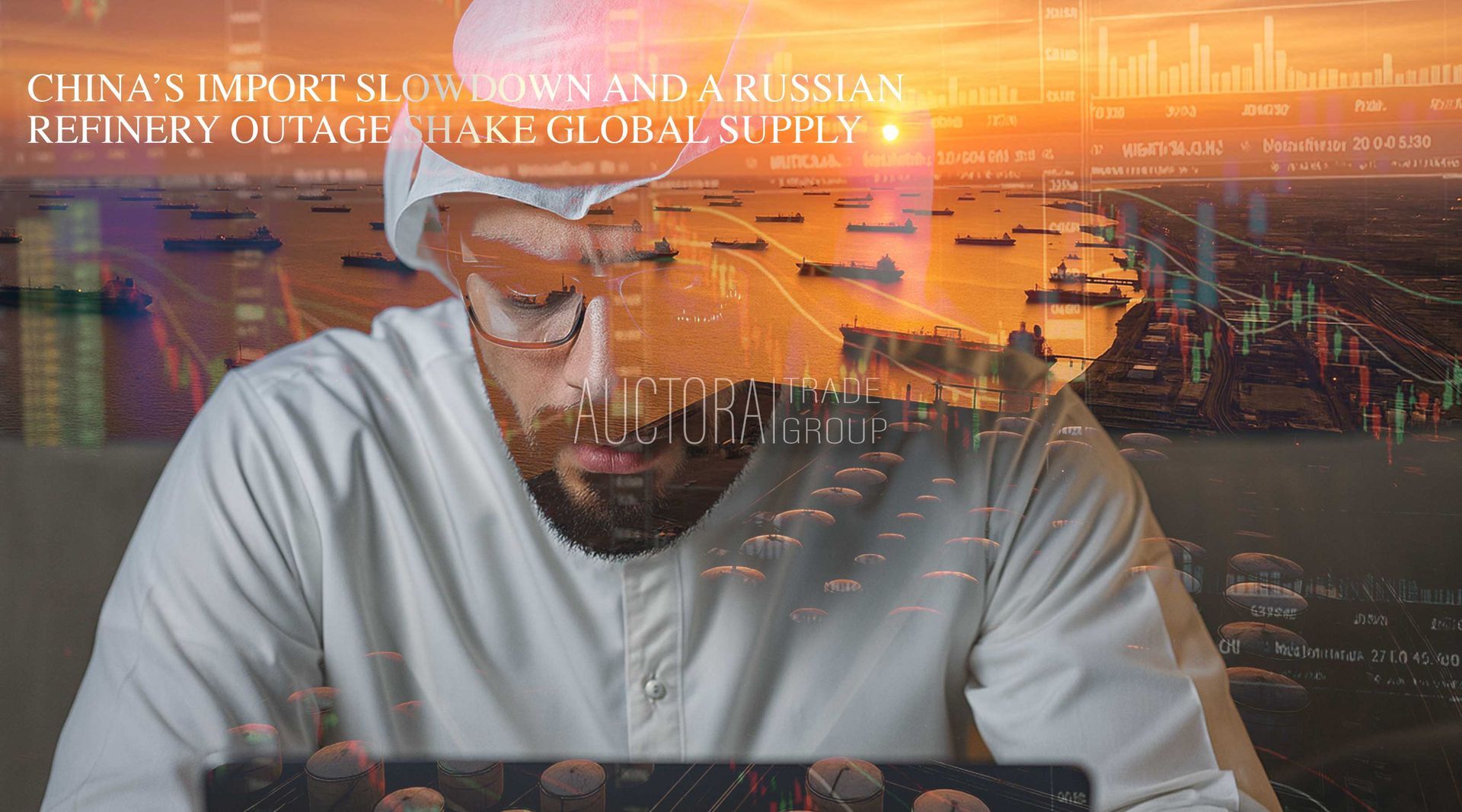

IEA Surplus Warning, China’s Import Slowdown and a Russian Refinery Outage Shake Global Supply Published in Abu Dhabi, 20 October 2025 2:56pm (GST) Over the past week oil traders have been pulled between two very different narratives. On one side, fears of a deep oversupply have dragged Brent and WTI to multi‑week lows, with benchmarks down more than two percent last week and early trades this week seeing Brent futures around US$61.11 and WTI near US$57.34 as investors priced in a looming glut. On the other side, geopolitical flashpoints continue to crop up, briefly tightening supply and reminding the market that refined products and crude flows can be interrupted without warning. At Auctora we see opportunity in the dislocation between these themes – but only for buyers and sellers prepared to adjust strategies quickly. The oversupply narrative gains momentum The International Energy Agency’s latest market update raised its forecast for global supply growth and warned that the world could be staring at a major surplus as soon as 2026. Analysts now expect non‑OPEC production to grow faster than demand, driven by the United States, Brazil and Guyana. At the same time, OPEC+ has been unwinding some of its output cuts, reversing course after nearly two years of restraint to regain market share from U.S. shale and other rivals. The Gaza ceasefire has further reduced concerns about supply disruption in the Middle Eastoilprice.com. Combined with an easing of U.S.–China trade tensions, these factors have encouraged selling pressure and pushed prices lower.

Energy markets brace for volatility as Fed cuts ripple through oil, trade routes, and global investment flows. Published in London, 22 September 2025 12:26am (BST) The oil market has taken investors on a roller‑coaster ride since the U.S. Federal Reserve cut rates by 25 basis points on 18 September. Initially traders hoped that cheaper borrowing would spur demand, but those gains were quickly erased as the focus shifted back to robust global supply and signs of weak demand. By the start of this week, Brent crude had slipped to about $66.57 per barrel, while WTI hovered around $62.64. Futures prices have remained locked in a narrow $65.50–$69 band since early August. This report dives into the key factors behind the latest price moves and what they mean for buyers, sellers and investors. We also provide actionable guidance drawn from our conversations with clients in London and across the Gulf Cooperation Council (GCC). Key Developments 1. Fed Rate Cut Fails to Lift Oil Demand • On 18 September the Federal Reserve delivered its first rate cut of the year, lowering its policy rate by 0.25 percentage points and signalling further reductions ahead. Normally a lower cost of capital would spur consumption and support oil prices. Yet the move came amid signs of a weakening U.S. jobs market and broader economic slowdown. • Traders quickly judged that a quarter‑point cut would do little to offset demand softness. Analyst John Kilduff of Again Capital said the Fed would need to be “more aggressive” to lift crude demand and warned that the central bank’s modest move could actually weaken the dollar, making oil more expensive for buyers. • Jobless claims have eased, but U.S. single‑family home construction plunged to a 2½‑year low. Both indicators point to headwinds for fuel demand. 2. Oversupply Fears Weigh on Prices • Despite OPEC+ rolling back some voluntary production cuts, global supplies remain ample. As Andrew Lipow of Lipow Oil Associates noted, “oil supplies continue to remain robust” and sanctions have yet to meaningfully disrupt Russian exports. • Iraq, the cartel’s second‑largest producer, increased exports as the OPEC+ quota unwind took effect. The state marketer SOMO expects September exports to reach 3.4–3.45 million barrels per day (bpd). • Kuwait’s oil production capacity has been assessed at 3.2 million bpd, its highest level in over a decade. This additional spare capacity hints at further supply pressure if demand remains lacklustre. • With supply growth outpacing consumption, analysts at SEB Bank warn that prices could slide into the $50s unless China opts to stockpile the surplus. 3. Distillate Stock Build & Refinery Turnarounds • U.S. distillate inventories rose by 4 million barrels in the latest weekly data, far exceeding expectations. The build reflects weak demand for diesel and heating oil. • The autumn refinery turnaround season is beginning, when refiners shut units for maintenance. According to Lipow, these overhauls will further reduce crude demand, amplifying the bearish sentiment. 4. Geopolitical Tensions but No Immediate Disruptions • Fresh tensions erupted as several Western nations recognised a Palestinian state and Estonia accused Russia of violating its airspace. While such events can spike risk premiums, they have not yet resulted in a meaningful oil supply disruption. • The Israeli strike in Doha earlier this month remains a concern for buyers; however, there has been no new escalation since, and Gulf export terminals continue to operate normally. Buyers should monitor the situation but avoid over‑reacting. 5. Other Energy News • In Kurdistan, Iraq’s government gave preliminary approval to resume pipeline exports through Turkey. A restart could add about 230,000 bpd to global flows once implemented. • Kuwaiti officials expect oil demand to rise following the Fed’s rate cut, especially from Asia. State‑owned QatarEnergy raised the term price for its al‑Shaheen crude to the highest level in eight months, signalling tight regional supplies for certain grades despite the broader oversupply narrative.

Energy Security in Focus as Regional Instability Rises Published in Abu Dhabi - UAE, 10 September 2025 2:15pm (GMT) On 9 September 2025, Israel carried out airstrikes in Doha, Qatar, claiming it targeted Hamas leadership. The strikes drew rapid international condemnation from the UN, EU member states, and Gulf capitals, and added a fresh layer of geopolitical risk in the Gulf. For now, operations across the region remain intact. Oil prices briefly rose by 0.5–2% on the headlines before pulling back after official guidance suggested no immediate escalation. The real impact lies in risk perception: freight spreads, war-risk premiums, and insurance are now centre stage, even as physical flows remain stable. What Happened Strike in Doha (9 Sept): Multiple explosions hit Doha. Israel claimed it targeted Hamas leaders; Qatar called the strike a violation of sovereignty. Fatalities were reported among Hamas members and security personnel. International Reaction: UN Secretary-General condemned the strike as a breach of sovereignty. UAE expressed solidarity with Qatar; Saudi Arabia called it a “criminal act.” Turkey pledged support to Doha. UK and Germany labelled the strike destabilising and unacceptable. Qatar’s Prime Minister vowed to continue Doha’s mediation role. Key takeaway: Political fallout has been swift, while operations remain steady a reminder that in commodities, risk is re-priced before it is realised.

EU Deforestation Rules and Agricultural Exports: What Buyers Need to Know Published in London, 29 August 2025 5:43pm (BST) The global agricultural commodities market is undergoing a major shift. With the European Union’s new anti-deforestation regulations coming into effect in December 2025, exporters of palm oil, soy, coffee, cocoa, and other key agricultural products will face tighter scrutiny when shipping into Europe. For buyers, traders, and brokers, this change isn’t just about compliance — it’s about positioning strategically in markets that are already showing signs of disruption. At Auctora Trade Group, we are working closely with our partners to ensure that sourcing strategies adapt quickly to this new regulatory environment. What’s Changing in Agricultural Commodities? The EU’s regulation will require proof that agricultural products entering the European market are not linked to deforestation. Countries are being risk-rated as: Low Risk (minimal checks on imports) Standard Risk (up to 3% of shipments checked) High Risk (up to 9% of shipments checked) At present, Malaysia — one of the largest exporters of palm oil and a key supplier to the Middle East — is classified as “standard risk.” Unless it is reclassified to low risk, a percentage of all shipments into Europe will face additional inspection and certification.

Why the UAE is Attractive Right Now Published in Abu Dhabi - UAE, 18 August 2025 10:04am (GMT) The United Arab Emirates has long been a magnet for global investors, but today the opportunities are greater than ever. For European businesses and international investors, the UAE offers not only stability but also the chance to become part of one of the fastest-growing, most ambitious economies in the world. Political and Economic Stability The UAE continues to rank among the most politically stable countries in the Middle East, giving investors confidence in long-term commitments. With GDP growth averaging 3.9% in 2024 and strong diversification away from oil, the UAE has become a resilient economy prepared for the future. Business-Friendly Policies 100% foreign ownership, zero personal income tax, and free repatriation of profits make the UAE one of the most open markets globally. Strategic Location Positioned between Europe, Asia, and Africa, the UAE serves as a natural hub for logistics, trade, and finance. Over 66% of the world’s population is reachable within 8 hours.

Shifting Supply, Tightening Contracts – Navigating Oil’s Uncertain Terrain Published in Abu Dhabi - UAE, 10 August 2025 17:35am (GMT)